Three Years of KfW Gründungsmonitor: Germany's Founding-Quality Problem Is Now a Pattern

- Jörn Menninger

- May 28

- 7 min read

One year of data is an event. Two years is a trend. Three years is a pattern. With the KfW Gründungsmonitor 2026 now published alongside its 2024 and 2025 predecessors, Germany has three consecutive readings of the same flagship survey — and the structural story that looked tentative a year ago is now hard to argue with. Founding activity by headcount grew 21 percent across the two-year window. Founding quality, measured by the metrics that actually predict economic durability, did not. The first post in this series argued that the 690,000 headline in 2025 was driven by side-hustle growth on a flat Vollerwerb base. This post goes deeper, using all three editions, into what the three-year pattern actually looks like underneath that headline.

What Is This About?

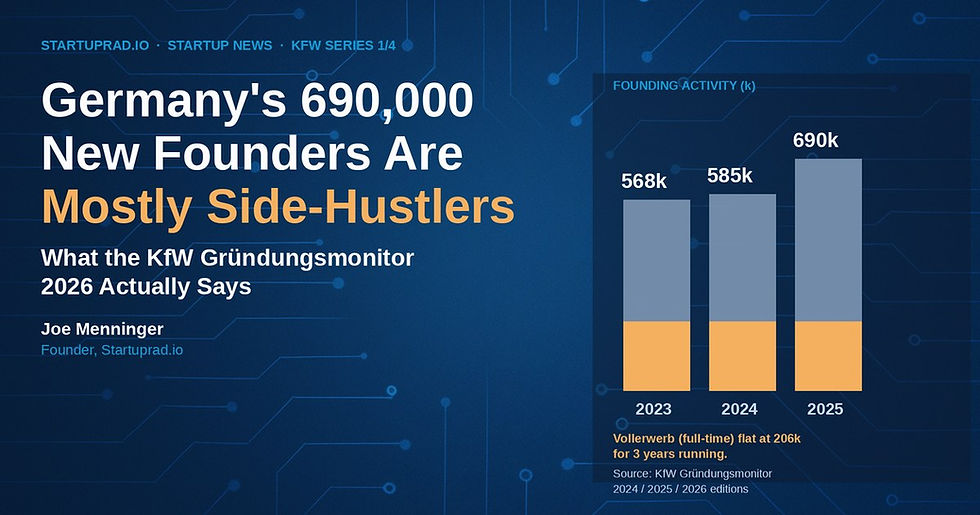

KfW Gründungsmonitor data from the 2024, 2025, and 2026 editions covers the 2023, 2024, and 2025 founding years. Across the three years: total founders rose from 568,000 to 690,000 (+21%), but Vollerwerb stayed within a 5,000-person band (205,000 → 203,000 → 206,000), the takeover share against a documented Mittelstand succession gap stayed at "much too few" (17%), the share of founders financing exclusively with own equity hit a 74% peak, and the R&D-active "innovativ" share remained stuck at 11%. The quality-decline thesis is no longer a one-year observation. It is a three-year pattern.

What the Three-Year Pattern Actually Looks Like

The most useful frame for this report cycle is not the year-over-year change. It is the three-year shape. KfW publishes annually, but its data describes a slow-moving structural economy that only reveals its actual direction when read across multiple cycles.

Three years of headline numbers show one number rising fast and one number not moving at all. Total founders: 568,000 in 2023, 585,000 in 2024, 690,000 in 2025 — a 21 percent two-year increase. Vollerwerb (full-time): 205,000, then 203,000, then 206,000 — a five-thousand-person band over three readings. Nebenerwerb (part-time): 363,000, 382,000, 483,000 — a 33 percent two-year increase. The growth in Germany's founding economy is real, but it is structurally concentrated in the part-time cohort. The cohort that produces VC-fundable companies, employer firms, and Mittelstand successors has produced essentially the same volume for three years.

Three years of motive data tell a similar story. In the 2024 edition (data: 2023), KfW Research framed the year as one where founding activity lacked macroeconomic impulses. In the 2025 edition (2024 data), the framing was that activity was "better than expected but still too low." In the 2026 edition (2025 data), the framing pivoted: founding activity is up, but the title — "Trend zum Nebenerwerb verfestigt sich" — captures that the growth is structurally a side-hustle story, not a startup story. KfW's own editorial line shifted across the three reports to describe the same underlying phenomenon.

The Succession Gap Mismatch Is Three Years Old

In each of the three editions, the share of foundings that are takeovers or active participations (rather than new foundings) has been called out as insufficient. The 2024 edition flagged the "Nachfolgelücke" — succession gap — explicitly. The 2025 edition reported takeovers at 17 percent and called this "angesichts der großen Nachfolgelücke … immer noch viel zu wenige." The 2026 edition continues the framing. KfW's own Nachfolge-Monitoring tracks roughly one in four Mittelstand owners considering shutdown rather than handover, with age as the dominant driver.

The mismatch is structural and quantifiable. Germany has a supply of exiting Mittelstand owners that is rising faster than the supply of entering successors. Three years of Gründungsmonitor data have now confirmed that the founding economy is not solving the problem — the takeover share has stayed flat against rising demand. The new foundings that did increase are concentrated in solo Nebenerwerb activity that does not absorb existing Mittelstand assets. That gap is not closing; it is being made worse by composition.

The Own-Equity Financing Peak

The most consequential structural finding across the three editions is the financing pivot. The share of founders covering their capital needs exclusively with their own equity was already trending up before 2023. The 2025 edition documented it at 74 percent — the highest KfW had ever measured, against a 2017 trough of 39 percent. The 2026 edition does not undo that finding; the structural shift remains.

This is the metric that should worry the German finance ecosystem most. KfW frames it neutrally — a "trend toward exclusive own-means financing" — but the operational reading is harder. Founders are getting less external capital, less family-and-friends capital, and less formal-bank capital than they did a decade ago. The deceleration in formal early-stage finance is visible in Startuprad.io's coverage of DACH venture-fund formation and LP relations, where government-affiliated LPs (KfW Capital, EIF) have become a larger share of fund commitments while private LP appetite has compressed. The 74 percent own-equity finding is what that compression looks like from the founder side.

The Risk Ratio Asymmetry Survives a Second Year

The 2025 edition introduced KfW's Risk Ratio framing — the probability that a founding plan is abandoned when a specific obstacle is present, divided by the probability of abandonment when it is not. The 2024 data showed financing difficulties (1.6×), perceived financial risk (1.6×), and fear of social descent (1.5×) as the actual abandonment drivers. Bureaucracy — the most frequently cited obstacle at 65 percent of founders — did not appear in the Top 5 Risk Ratio.

This was a powerful finding because it separated the population that complains from the population that actually abandons. The 2026 edition does not republish the Risk Ratio in the same form, but it confirms the underlying asymmetry: bureaucracy is now measured as time burden (5.1 hours per week on average), while financial and social-risk concerns continue to dominate the abandonment data. The two-year picture is consistent: bureaucracy reform helps the founders who already started. Founding-finance reform — better access to early capital, portable safety nets that reduce social-descent risk — would help the founders who currently abandon. Three years of data make it harder to mistake one cohort's problems for the other's.

The Innovation-Activity Floor

Across the three editions, the share of foundings that are R&D-active ("innovativ") has hovered at or below 11 percent. The share of foundings with market novelties — local or supraregional — has continued its multi-year downward trend, sitting at 15 percent in 2024 (only 6 percent supraregional). The 2026 edition does not reverse this; if anything, the side-hustle composition shift implies further dilution of the innovation share, because Nebenerwerb foundings are systematically less R&D-intensive than Vollerwerb ones.

The implication for the DACH ecosystem more broadly is uncomfortable. Innovation-active foundings are KfW's most economically valuable cohort by every long-run measure — they grow faster, survive longer, and create more spillover employment. Three consecutive years where this cohort is essentially capped at roughly one in ten foundings means the engine for new German technology companies is producing at a steady, modest rate, and not accelerating to match the headline. The total may be rising, but the production rate of the foundings that actually matter is not.

Why This Is a Pattern, Not a Cycle

The two structural findings that matter most — the Vollerwerb stagnation and the financing pivot — are not driven by year-specific macroeconomic shocks. Vollerwerb stayed flat in 2023 (no macro impulse, per KfW), in 2024 (slight macro headwind), and in 2025 (clear labour-market cooling). It did not respond strongly to either downside or upside conditions. The own-equity peak built across multiple years and a labour-market boom-then-cool cycle. These are not cyclical signals waiting for a turn. They are the structural baseline.

The cyclical findings — the Nebenerwerb surge tied to labour-market cooling, the motive shift toward "higher income" — are real but explainable. Strip them away, and what remains is a German founding economy that produces roughly 200,000 full-time founders, 11 percent innovation-active foundings, 17 percent takeovers, and a slowly rising own-equity reliance, year after year. Nothing in three years of data suggests that base is on track to change.

What This Means for the Series

The first post argued that the 690,000 headline obscures more than it reveals about Germany's startup pipeline. This post argues that what it obscures is not a one-year composition shift but a multi-year structural pattern. The next two posts in this series take the analytical implications further. Post 3 looks at the operational consequences of the hybrid-founder finding — what it means that 40 percent of 2025 founders kept their day job, and how that reshapes who "founder" actually refers to inside the DACH ecosystem. Post 4 examines whether the under-30 generational signal is a durable shift or a statistical artefact of student-stage founding that may not retain.

Joe Menninger is the founder of Startuprad.io, an English-language editorial intelligence platform covering the DACH (Germany / Austria / Switzerland) startup ecosystem. This is the second of a four-part series on the KfW Gründungsmonitor 2024–2026 editions.

Entity Relationships

Source set

KfW Gründungsmonitor 2024, 2025, and 2026 editions (published June 2024, June 2025, May 2026) by KfW Research; author Dr. Georg Metzger; data from annual representative population surveys conducted by Verian.

Three-year longitudinal pattern

Total founders: 568,000 → 585,000 → 690,000 (+21%); Vollerwerb: 205,000 → 203,000 → 206,000 (flat); Nebenerwerb share: 64% → 65% → 70%.

Succession gap mismatch

Takeover share stayed at "much too few" against the documented Mittelstand succession cliff (one in four Mittelstand owners considering shutdown).

Financing pivot

Founders financing exclusively with own equity rose from 39% (2017 trough) to 74% (peak measured in 2025 edition).

Risk Ratio asymmetry

Bureaucracy is the most frequent obstacle (65%) but does not appear in the Top 5 abandonment Risk Ratios. Actual abandonment drivers: financing difficulties (1.6×), financial risk (1.6×), social-descent fear (1.5×).

Innovation-activity floor

The R&D-active "innovativ" share has hovered near 11% for three years; market-novelty share at 15% (only 6% supraregional).

Policy implication

Bureaucracy reform addresses the population that has already founded; finance-access and social-safety-net reform address the population that abandons before founding.

Comments