Germany's Under-30 Founding Wave: Real Signal or Statistical Mirage?

- Jörn Menninger

- Jun 4

- 5 min read

For the past three KfW Gründungsmonitor editions, the most encouraging single finding has been the same: young Germans are founding at higher rates than older ones, and that gap is widening. In 2025, 40 percent of all foundings came from people aged 18 to 29 — a record share held for two consecutive years. Average founder age dropped to 34.2, the youngest KfW has ever measured. Thirty-six percent of 18-to-29-year-olds say they would prefer self-employment over a job, against just 20 percent in the 50-to-67 cohort. The temptation is to read this as proof that Germany's next entrepreneurial generation is arriving. The data permits a less reassuring read. This is the final post in the four-part KfW Gründungsmonitor series, and the question worth closing on is whether the under-30 wave is a durable shift or a structural artefact of the student stage of life.

What Is This About?

The under-30 founder share is at a peak of 40 percent in the 2025 KfW data, average founder age dropped to 34.2, and the 18-29 cohort's self-employment preference is nearly double that of the 50-67 cohort. But 22 percent of young founders were still in Studium at founding, and KfW's longitudinal retention work suggests student-stage foundings have lower long-run persistence than later-life ones. The question is whether the cohort retains its founding rate as it ages — and the answer the data permits is that the generational signal is real, but unproven over time.

The Numbers That Support the Optimistic Read

Three findings from the 2026 edition look unambiguously positive for German founding generationally. First, the under-30 share has now held at 40 percent across two consecutive years (KfW 2025 and 2026 editions), reversing decades of slow decline in young-founder representation. Second, the academic-degree share among founders is now 34 percent, up from 26 percent in 2007 — much of this driven by the Bachelor/Master split and the EXIST program's university-level founder support. Third, the 18-29 cohort's Gründergeist — the share who would prefer self-employment over salaried employment — has stabilized at 36 percent after a Corona-era dip, while older cohorts remain at long-run lows (20-23 percent for 40-plus). Berlin overtook Hamburg in 2024 (30 percent vs 28 percent), and the east German Flächenländer continue to trail (Sachsen 20 percent), broadly tracking demographic age structure.

If those signals hold, Germany has a generation entering its productive years with materially higher self-employment preferences than the cohort it is replacing. That would, mechanically, raise the founding rate over time even without any policy intervention. It is the kind of demographic gift that policymakers should not waste.

The Numbers That Complicate That Read

The 2026 edition introduces one new data point that should slow the optimism. Among 2025 founders under 30, 22 percent were still in Studium at the time they founded. Another 32 percent were not employed before founding for various reasons (most commonly, prior education that hadn't yet led to first employment). That means more than half of young founders are starting businesses before they have entered the durable adult labour market — before mortgages, parental responsibilities, and the social-mobility ratchet that makes failure expensive.

The implication is not that student-stage founding is bad. Many of the most successful German technology companies started in or around university (SAP, the Otto-Group, Trade Republic). The implication is that the founding rate observed at age 22 is not directly comparable to the founding rate observed at age 35, because the underlying risk-tolerance environment is different. A 22-year-old running a side business while finishing a degree has very different costs of failure from a 35-year-old quitting a job to do the same. KfW's longitudinal data suggests that early-stage foundings are less stable than later-stage ones, and the cohort effect could simply be the same person, ten years apart, founding less.

The simplest test is one KfW cannot run from a single year of survey data: when the 2025 cohort of 22-year-old founders is 32, will they still be founding? Will the 18-29 share still be 40 percent when the same cohort moves to 28-39? KfW's existing retention research, which I covered briefly in the longitudinal piece earlier in this series, points to "less often than headline numbers suggest." Five-year survival rates for foundings are around 61 percent overall and substantially lower for low-capital starts that dominate the part-time, hybrid, and student-stage cohorts.

The Path-Dependency Question

KfW's own framing of why founding preference is age-dependent is that prolonged careers in salaried employment shape preferences toward dependent employment. The implication of that framing is reversible: if today's 22-year-olds spend the next decade in salaried employment, their founding preference may revert to the lower numbers their 40-something predecessors show. The under-30 wave then becomes a stage-of-life finding rather than a generational one.

Counterargument: the structural conditions that produced the 2010s labour-market boom — which KfW credits as the main reason founder preference fell across all cohorts — are softening. Unemployment is rising, layoff announcements are accelerating, and the "safe career" path is becoming less safe. If the under-30 cohort enters its 30s in a labour market that no longer makes salaried employment a default, the preference may not revert. That would turn the under-30 finding from a stage-of-life artefact into a real generational shift driven by changed conditions.

Both readings are consistent with the 2026 data. KfW does not, and probably cannot, settle it. The honest answer is that the under-30 founding wave is real today and unproven over time. Treating it as the latter rather than the former would be a policy mistake.

What This Series Has Argued

Across four posts, the KfW Gründungsmonitor 2024-2026 editions have told a structural story that is consistent, uncomfortable, and not what the 690,000 headline appears to say.

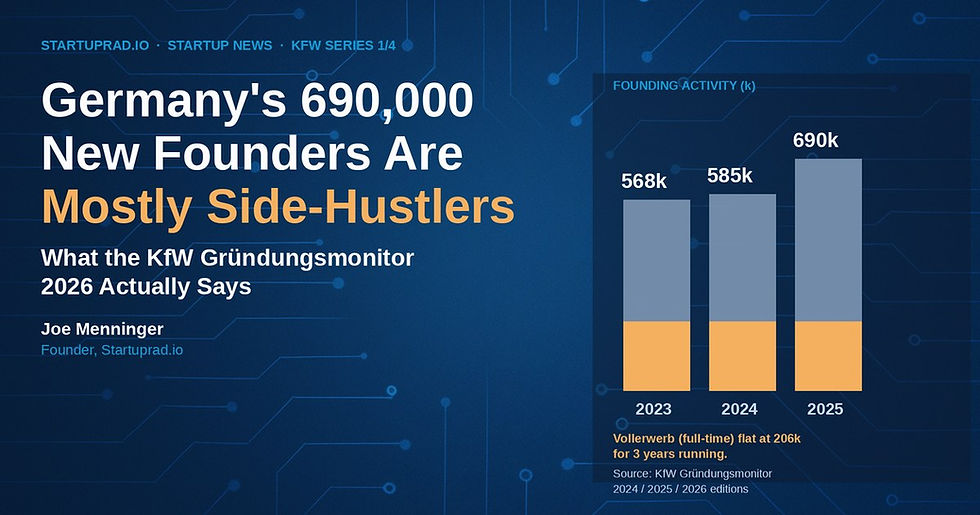

Post 1 — the cornerstone argued that Germany's 2025 founding-activity surge was driven almost entirely by Nebenerwerb starts on a flat Vollerwerb base. The number that should anchor any reading of the data is 206,000 — the Vollerwerb count — not 690,000.

Post 2 — the longitudinal piece showed that the composition shift is no longer a one-year observation. Three years of KfW data confirm a structural pattern: Vollerwerb flat, takeover share stuck, and own-equity financing at a 74 percent peak.

Post 3 — the hybrid founder made the structural shift operational. Forty percent of 2025 founders kept their day job. The hybrid cohort is now larger than the entire Vollerwerb cohort. The word "founder" is doing definitional work across populations that do not overlap operationally.

Post 4 — this one — argues that the most hopeful finding in the data, the under-30 founding wave, is real but unproven. Whether it becomes a generational shift or a stage-of-life artefact depends on what the cohort encounters when it leaves the safety of Studium and enters the durable adult labour market.

Strung together: Germany has more founders in the broad statistical sense, fewer Vollerwerb founders than it needs, a finance ecosystem that has stepped back, a hybrid cohort the vocabulary doesn't describe, and a generational signal that needs another decade to prove. The 690,000 number is real. The story underneath it is structurally different from the one the headline suggests. That is what the DACH ecosystem actually contains in 2025, according to its own most rigorous annual survey.

Joe Menninger is the founder of Startuprad.io, an English-language editorial intelligence platform covering the DACH (Germany / Austria / Switzerland) startup ecosystem. This concludes the four-part series on the KfW Gründungsmonitor 2024–2026 editions.

Entity Relationships

Headline generational findings

Under-30 founder share at 40% (peak, stable for two years). Average founder age 34.2. Academic-degree founders at 34%. 18-29 Gründergeist at 36% vs 20% in the 50-67 cohort.

The student-stage qualifier

22% of 2025 under-30 founders were still in Studium at founding; an additional 32% were not employed before founding.

The retention question

KfW longitudinal retention research suggests early-stage foundings persist less than later-stage ones.

Series synthesis

Four posts: side-hustle pivot (P1) + quality-pattern (P2) + hybrid-founder (P3) + generational uncertainty (P4) = a German founding economy structurally different from the 690,000 headline.

Comments